Is Life Insurance Really a Safety Net or Just an Additional Expense?

When considering if life insurance serves as a genuine safety net or merely an additional expense, it's essential to evaluate its potential benefits. First and foremost, life insurance provides financial security for your loved ones in the event of your untimely passing. This coverage can prevent them from falling into financial hardship, as it can replace lost income, cover outstanding debts, and even fund future expenses like education. With various policies available, individuals can tailor coverage to suit their specific needs, thus making it a foundational component of financial planning.

On the flip side, some view life insurance as just another recurring cost that doesn't yield immediate benefits. Monthly premiums can strain a budget, especially for those who feel invincible in their health and young age. However, it's crucial to recognize that life insurance is not solely about immediate returns; it's about long-term security and peace of mind. The question ultimately hinges on your financial situation and obligations—if you have dependents relying on your income, life insurance transitions from being an expense to a priceless safety net.

Understanding the True Value of Life Insurance: A Comprehensive Guide

Understanding the true value of life insurance involves recognizing its primary purpose: providing financial security for your loved ones in the event of your untimely passing. It acts as a safety net, ensuring that your family's financial obligations, such as mortgage payments, education expenses, and daily living costs, are taken care of. Moreover, life insurance can serve as a strategic part of your financial planning, offering a range of benefits such as tax advantages, cash value accumulation, and peace of mind knowing your loved ones are protected.

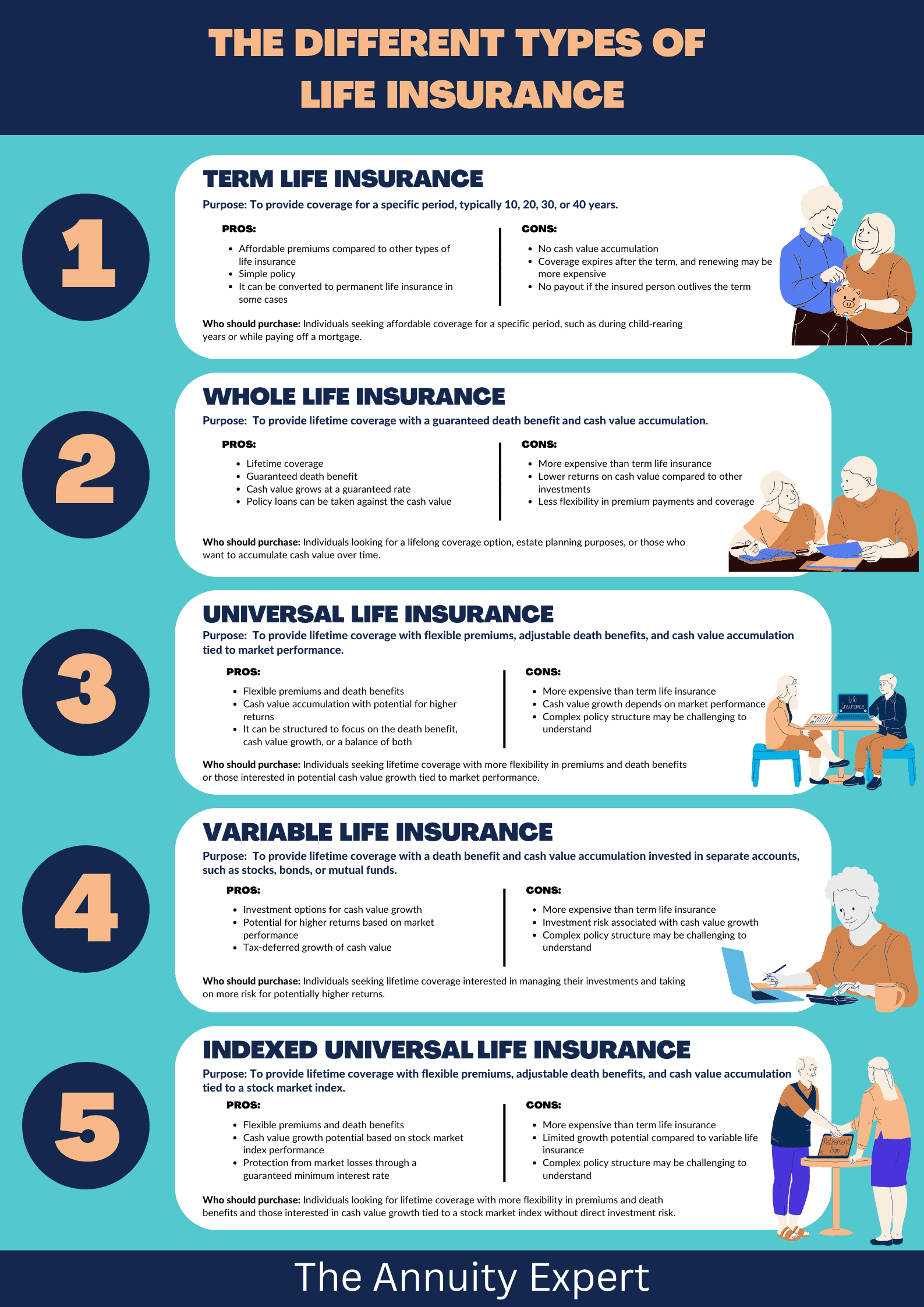

There are different types of life insurance policies, each tailored to various needs and circumstances. Term life insurance provides coverage for a specified period, while whole life insurance offers lifetime protection with a cash value component. Consider these options carefully, and assess your personal situation by asking questions such as:

- What are my financial responsibilities?

- Who relies on my income?

- What is my budget for premiums?

5 Common Misconceptions About Life Insurance Debunked

Life insurance is often surrounded by myths and misconceptions that can lead to confusion and hesitation. One common misconception is that it's only necessary for older individuals or those with dependents. In reality, life insurance can be beneficial for younger individuals as well, especially if they have debts, a mortgage, or plans for future financial responsibilities. The earlier you get life insurance, the lower your premiums can be, offering you peace of mind while securing your financial future.

Another frequent myth is that life insurance is too expensive. While costs can vary based on factors like age and health, there are plenty of affordable options available. Many people avoid considering life insurance due to perceived high costs, yet over half of Americans mistakenly believe they need more coverage than they truly do. Regularly assessing your needs can help you find a life insurance policy that fits your budget and provides the necessary protection.